If you run a small business, you already know that keeping your finances in order is not optional. But one task that many business owners either delay or skip entirely is bank reconciliation, and that is a mistake that can quietly cause serious problems.

This bank reconciliation guide is designed to make the process simple, clear, and manageable, whether you are doing it yourself or working with a professional team. Understanding bank reconciliation for small business owners is the first step toward keeping your finances accurate and stress-free.

What is Bank Reconciliation? A Simple Guide

Bank reconciliation is the process of comparing your business’s internal financial records with your bank statement to make sure they match. Every transaction that appears in your accounting software or ledger should also appear on your bank statement and vice versa.

When the two records match, your books are accurate. When they do not, there is a discrepancy that needs to be investigated and resolved.

It’s like a regular check-up for your financial health. Just like you would not ignore unusual symptoms in your body, you should not ignore mismatches in your financial records. A structured bank reconciliation process helps you catch problems early before they turn into bigger issues.

Why Bank Reconciliation is Important for Small Businesses

Many small business owners view bank reconciliation as a chore. But the reality is that it is one of the most important financial habits you can build. Here is why:

Catch Errors Early

Mistakes happen, whether it is a duplicate transaction, an incorrectly recorded amount, or a bank error. Regular reconciliation catches these before they compound into larger problems.

Detect Fraud

Unauthorised transactions, suspicious charges, or unusual payment patterns show up during reconciliation. Catching them early protects your business from financial loss.

Accurate Cash Flow Visibility

When your books match your bank statement, you always know exactly how much money your business has. This is essential for planning, budgeting, and making smart financial decisions.

Stay Tax Ready

Clean, reconciled books make tax preparation significantly easier. When combined with outsourced tax processing services, your accountant or CPA will have accurate data to work with, reducing the risk of errors and saving time.

Audit Confidence

If your business is ever audited, well-maintained reconciliation records show that your finances are managed professionally and accurately.

Types of Bank Reconciliation

Not all reconciliation is the same. Here are the main types of small businesses that typically need to be managed:

Bank Statement Reconciliation

The most common type is comparing your bank statement with your accounting records to ensure all deposits, withdrawals, and charges are recorded correctly.

Bank and credit card reconciliation

Involves matching credit card statements with recorded expenses to verify that all card payments, refunds, and charges are accurately captured in your books.

Cash Reconciliation

For businesses that handle physical cash, this involves comparing cash register records with actual cash on hand to identify any shortfalls or surpluses.

Intercompany Reconciliation

For businesses with multiple entities or subsidiaries, this ensures that transactions between related companies are recorded consistently on both sides.

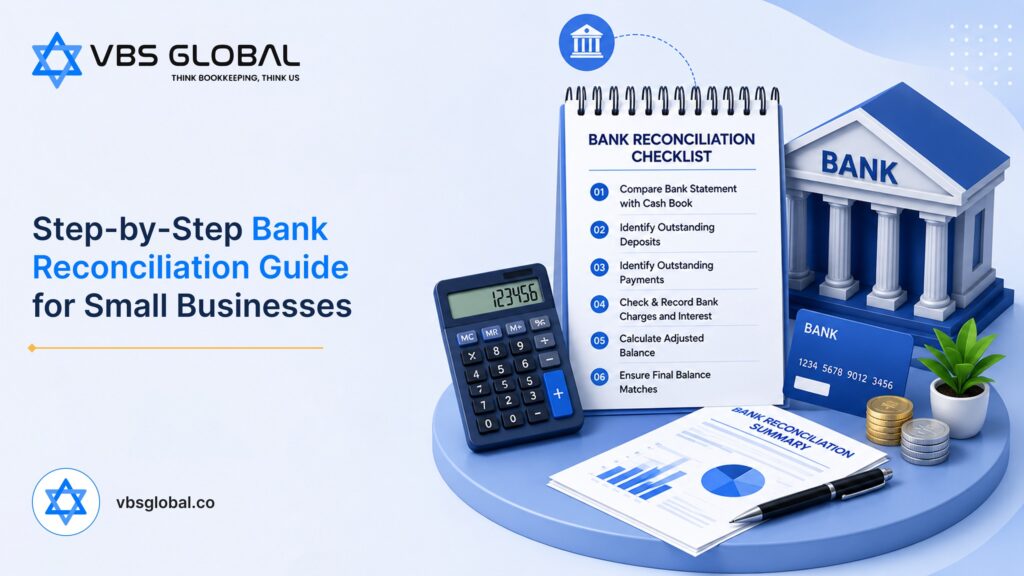

Step-by-Step Bank Reconciliation Guide: The Complete Process

This is the core of any bank reconciliation guide. Follow these seven steps to reconcile your bank accounts accurately every time.

Gather bank statements and records

Start by collecting everything you need:

- This is your bank statement for the period being reconciled.

- Your accounting software report or general ledger for the same period.

- Any receipts, invoices, or payment records for reference.

Having everything in one place before you start saves time and reduces the chance of missing something important.

Compare Opening Balances

Check that the opening balance in your accounting records matches the opening balance on your bank statement. If these do not match, there may be an unresolved issue from the previous period that needs to be addressed first. This step is often overlooked, but starting with mismatched opening balances means your entire reconciliation will be off.

Match Deposits and Credits

Go through every deposit on your bank statement and match it with a corresponding entry in your accounting records. This includes:

- Customer payments received

- Bank interest credited

- Refunds deposited

Tick off each matching item. Any deposit on the bank statement that is not in your records or vice versa needs to be investigated.

Match Withdrawals and Payments

Now match every withdrawal, payment, and debit on your bank statement with your accounting records. For businesses using accounts payable outsourcing, your provider will typically handle this matching as part of their service. This includes:

- Supplier payments

- Direct debits and standing orders

- Bank charges

- Tax payments

Again, tick off each matching item and flag any that do not match.

Identify Discrepancies

After matching all transactions, some unmatched items may remain, called discrepancies. These include outstanding checks, deposits in transit, bank errors, timing differences, and missing entries. Each discrepancy should be carefully reviewed and verified. Finally, they must be corrected or explained to maintain accurate financial records.

Make Adjusting Entries

For any discrepancies that require correction, make the necessary adjusting entries in your accounting system. This might include:

- Recording bank charges that were not previously entered

- Adding missing transactions

- Correcting amounts that were entered incorrectly

Always document the reason for each adjustment. This creates a clear audit trail and makes future reconciliations easier.

Confirm Closing Balances

Once all adjustments are made, confirm that the closing balance in your accounting records matches the closing balance on your bank statement. If they match, your reconciliation is complete. If they do not, go back through the steps to find the remaining discrepancy. A completed reconciliation with matching closing balances means your books are accurate and up to date.

Common Bank Reconciliation Mistakes to Avoid

Even with a clear process in place, mistakes happen. Here are the most common ones that small businesses often commit, and tips to prevent making the same mistakes:

- Delaying reconciliation

The longer you leave reconciliation, the more transactions pile up and the harder it becomes to find errors. Month-end close review services help businesses stay on track, ensuring reconciliation is completed on schedule every month without falling behind. - Ignoring small discrepancies

It is tempting to ignore small differences. Do not. Even a small discrepancy can indicate a recurring error or unauthorized transaction that will grow over time. - Mixing Personal and Business Finances

Having one account for personal and business purposes causes problems with reconciliations and tax issues. Always keep them separate. - Missing supporting documents

Every transaction should have a supporting document, a receipt, an invoice, or a payment confirmation. Without these, it is impossible to verify transactions during reconciliation. - Relying on Memory

Never assume you know what a transaction was without checking. Always verify against the source document.

How Often Should Small Businesses Do Bank Reconciliation?

The short answer as often as possible.

- As part of small business bookkeeping, monthly reconciliation helps keep records accurate and up to date.

- Weekly reconciliation suits high-transaction businesses like retail, ecommerce, and hospitality.

- Daily reconciliation is used by cash-heavy or high-volume businesses such as restaurants and fast-moving retailers.

The key rule is simple: the more transactions your business processes, the more frequently you should reconcile. Leaving reconciliation for too long can lead to errors, stress, and inaccurate financial reporting.

Tools Used for Bank Reconciliation

Modern accounting tools make bank reconciliation significantly faster and more accurate. These are some of the most commonly used platforms.

- QuickBooks: Online automatically imports bank transactions and matches them with recorded entries, reducing manual work and making reconciliation much faster.

- Xero: Known for its excellent bank feed integration, Xero automatically pulls in transactions and highlights unmatched items for review.

- Zoho Books: A cost-effective option that offers solid bank reconciliation features suitable for smaller businesses looking for an affordable cloud-based solution.

Do You Need Outsourced Bank Reconciliation? Key Signs

Managing reconciliation in-house works for some businesses, but there are clear signs that outsourcing might be the better option:

- Always Behind: If your reconciliation is regularly weeks or months overdue, your financial data is not accurate and that creates risk.

- Unexplained Differences: Recurring discrepancies that you cannot track down suggest your process is not thorough enough.

- Reconciliation Takes Too Long: If you are spending hours every month on reconciliation instead of running your business, it is time to delegate.

- Business Is Growing: More transactions equal more complex processes. As your business scales, reconciliation becomes harder to manage without specialist support.

- Tax filing errors: If reconciliation errors have caused problems at tax time, outsourced accounting services can ensure it does not happen again with professional teams managing your books accurately year-round.

How VBS Global Helps With Bank Reconciliation

At VBS Global, we provide professional bank reconciliation outsourcing services for small businesses across the UK and Australia. As one of the trusted outsourced accounting firms offering bank reconciliation services USA wide, our team handles every step of the reconciliation process from matching transactions and identifying discrepancies to making adjusting entries and preparing clear monthly reports.

Working with us means:

- Accurate monthly bank and credit card reconciliation.

- Clear reconciliation reports are prepared for every period.

- Early identification of errors, duplicate entries, and discrepancies.

- Cloud-based reconciliation using QuickBooks, Xero, and Zoho Books.

- Dedicated support from a qualified bookkeeping team.

- Secure data handling with strict confidentiality protocols.

Whether you need help getting your reconciliation back on track or want a reliable team to manage it on an ongoing basis, VBS Global is ready to help.

At VBS Global, we help small businesses stay accurate, organized, and financially stress-free. Book a Free 30-Minute Consultation and let our team handle your bank reconciliation today.

Conclusion

Bank reconciliation might not be the most exciting aspect of running a small business, but it is one of the most crucial. A reliable bank reconciliation guide gives you the process and confidence to keep your books accurate, catch errors early, and make better financial decisions.

Whether you manage reconciliation in-house or work with a professional team, the commitment to doing it regularly and doing it right is one of the smartest financial habits your business can build.

If you are ready to take the stress out of bank reconciliation, VBS Global is here to help.

FAQ

1. How long does bank reconciliation take for a small business?

It depends on transaction volume and how up-to-date your records are. For most small businesses, monthly bank reconciliation takes around one to three hours when done regularly. If records are delayed, it can take much longer.

2. What should I do if my bank reconciliation does not balance?

Go through each step carefully by checking opening balances and reviewing unmatched transactions. Look for timing differences or missing entries in your records. If the issue remains, a professional bookkeeper can help identify and fix it.

3. Can I do bank reconciliation without accounting software?

Yes, it is possible to do manually without software, but it is time-consuming and more prone to errors. Tools like QuickBooks and Xero automate matching and reduce mistakes. This reduces the processing time, and its precision is increased.

4. What is the difference between bank reconciliation and bookkeeping?

Bookkeeping involves recording all financial transactions regularly. Bank reconciliation is a specific process that matches those records with your bank statement. Both work together to ensure accurate financial reporting.

5. How does outsourced bank reconciliation work?

An outsourced team accesses your accounting software and bank data through secure platforms. They perform reconciliation regularly and ensure all records match correctly. You receive reports with updates, discrepancies, and necessary adjustments.